The 4 Strategies in Public Safety Tech

Mission: To Survive and Sustain

Hi,

Welcome to Roll Call, a newsletter about the state of policy and technology in public safety, and the people shaping it. If you’d like to sign up, you can do so here. Or just read on…

TL;DR

PSaaS (Public Safety as a Service) - commitment to the entire CFS lifecycle and to software exclusively.

Vertical Value - build hardware that first responders can’t live without (radio, bodyworn camera, etc.), the software to support/manage, and expand into other parts of CFS lifecycle.

Comms Curator - available to a small handful of cos that (1) have accreditative power and (2) are true platforms for real-time and mission critical operations. Leverage status as base layer to curate a selection of recommended products for agencies. Smaller companies can use platform as crutch.

Buddy or Bust - Software or hardware that addresses one part of the CFS lifecycle. Can eke out existence as small player, aim to be acquired, or partner with other focused companies to expand impact.

Multiple strategies can be employed at once to fuel growth and increase the chance of long term company survival.

Today’s note covers the strategies being employed by ambitious public safety tech companies. Each has advantages and weaknesses. It will help to define each of these strategies visually, using a simplified modern duty belt as the foundation:

PSaaS

Other companies do it, and we’ll name them later, but SOMA Global gets to be linked to PSaaS because they market it the best. You claim the title, you get the free exposure. A pure software player that pitches itself as a platform, SOMA claims that they are a one-stop-shop for all of an agency’s software needs.

The above diagram goes a bit beyond SOMA’s capabilities, at least today, but shows the pieces that are important to be considered a full PSaaS. The biggest expenses are CAD and RMS, and the integration between those two in particular is critical. Only the largest agencies will buy from different vendors because they are the only ones with the personnel and money to spend on exhaustive selection and deployment processes. So, paradoxically, you need to do more to win the smallest agencies; a conundrum unique to public safety.

Below are the four parts of SOMA’s PSaaS, plus a mobile component to CAD and data interoperability. The core of any PSaaS is going to be CAD-RMS-JMS: that covers everything from the beginning of an incident to managing the health of inmates.

The goal of a PSaaS company is to cover everything from pre-incident through the criminal justice process with software. Note that this doesn’t preclude a company from building hardware, but only requires that a company Condensed and mapped to the CFS lifecycle, it looks like this:

Value to Agency:

Only One - need to select just one main provider for several of the riskiest and most mission-critical systems. Put delicately by some agency tech leaders as “one throat to choke.”

Bundled products lead to discounts.

Integration - guaranteed* for products within suite (e.g. CFS data should be available way down the line in evidentiary systems).

* not always, because legacy providers can suck at integrating new acquisitions, on-premise solutions (as opposed to cloud-first) can struggle to reconcile outdated versions, and other complications

Company Strengths:

Software’s natural advantage of high margins.

Building configurability into the products enables PSaaS companies to minimize deployment cost, because agencies are able to build around their own workflows and go live at own pace.

Organic market; small agencies don’t have resources to look for 10 different products. Full software suites help save time and effort hunting for solutions.

Company Vulnerabilities:

Pulling it off is operationally brutal. Can stretch a company thin. Engineering talent, or capital for acquisitions, needs to be spread over multiple products. This causes delays and integration challenges

No stickiness from hardware lock-in. If there’s LMR infrastructure set up or a bodyworn video program (as we’ll see in next section), capital expenditures will weigh on the mind. Sunk costs are a real force in the public sector.

Switching costs are low. This is offset somewhat by the length of procurement cycles, which intimidate agencies into continuing with ill-fitting software for too long.

Big opportunities are tough to win: large agencies looking at full software suites tend to have many needs, which means RFPs can become a feature checklist battle.

Who’s Doing It

Central Square - Top Tier

Tyler Technologies - Top Tier

SOMA Global - Close Second Tier

Mark43 - Aspiring

Kaseware - Aspiring

Motorola Solutions - Honorable Mention (better example of next category)

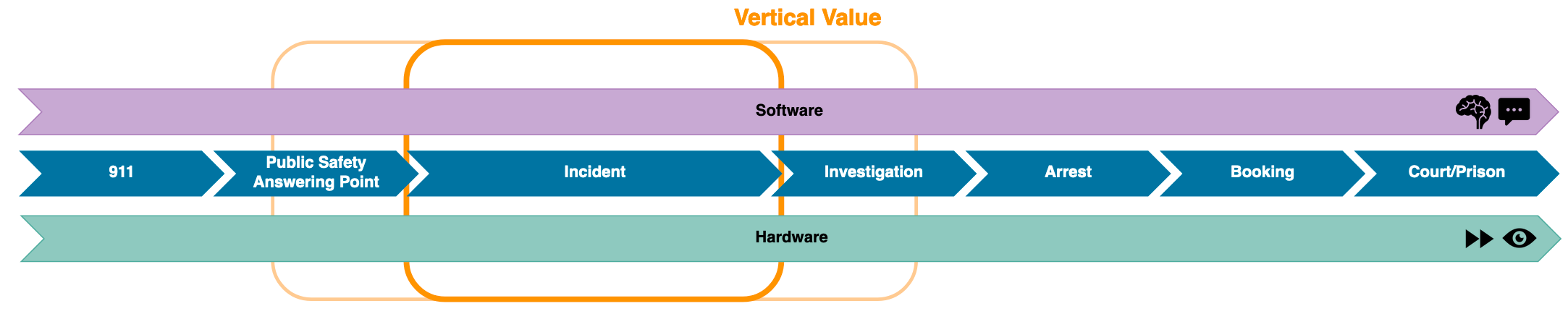

Vertical Value

The two best examples of vertical value are Motorola Solutions and Axon. Each builds software that is locked in place by even more powerful hardware. This is an inversion of the traditional Silicon Valley hierarchy with software at the top. My hypothesis is that this inversion happens because of old-school, local government procurement process norms, where cap-ex hardware purchases require more justification on average than op-ex subscription payments. In public safety, the SaaS op-ex can be mentally written off more easily than the capex purchase orders. As mentioned above, the sunk cost fallacy punches above its weight in public safety.

In effect, combining software and hardware dramatically increases the value of a solution. In rare cases, this leads to companies building a product that dominates the market. Motorola owns ~85% of the public safety two-way radio (LMR) market. Roughly 70% of sworn officers carry a Taser. That depth of market penetration enables higher margins, which fund expansion into adjacent product categories. Motorola has moved into a wide swath of adjacent tech and services, from call handling to video surveillance to RMS to analytics. Axon is using its Taser and bodyworn video platform to build dispatch and records solutions.

Value to Agency:

Bundled products lead to discounts. The adjacent products are usually aggressively priced.

Investment in the Future - If you squint really hard, you could say that over-paying for product leaders can be thought of as an investment in other future-oriented technology. Takes a lot of irritation to build pearls; Motorola and Axon in particular have well-oiled sales channels and significant patent protection that buttress their high prices on category leading products.

Company Strengths:

Land and expand. Establish value by owning one part of CFS lifecycle, use the margins to fund development of adjacent products and services. Those offerings can be equal or higher quality and lower cost than competitors, because you can give away margin to increase sales. It’s a way of having your cake and eating it too.

Company Vulnerabilities:

Difficult to do - need to be clear leader in a necessary product category to build high margins.

Agencies know when companies do this and can feel trapped.

Who’s Doing It

Motorola Solutions - Top Tier

Axon - Top Tier

ShotSpotter - Second Tier

RapidDeploy - Aspiring (a hardware component in the Emergency Data Gateway box as part of dispatch solution)

Utility - Aspiring (bodyworn video and in-car video, announced recent expansions into ALPR and gunshot sensors)

Comms Curator

The position of curator is least defined and most interesting. There are two functions that are foundational to public safety tech:

Real-time communication, traditionally addressed through LMR but increasingly by LTE.

Software hosted in the cloud

This means that carriers and cloud infrastructure providers have incredible leverage over public safety tech companies. Almost all agencies rely on some combination of AT&T FirstNet, Verizon Public Safety, Microsoft Azure, and Amazon AWS. As cloud-based dispatch and records software becomes the norm, this will be universal. Each of those four builds secure and reliable systems at huge cost to comply with state and federal requirements. Taking on that burden earns massive contracts with mission critical software companies, and earns the trust of agencies that rely on those tools every day. Trust begets authority. The telecom and cloud providers can set the terms of their relationships with tech companies, which means they can (formally or informally) accredit, recommend, or resell. They can also discredit, advise against, and occasionally veto.

This small cabal of companies can remain neutral. But they might not. If they don’t, they can use their leverage to curate a selection of companies with which they prefer doing business, can even resell bundles of products across companies, or can promote ventures that they’ve incubated and release them to a massive audience. On the flip side, a small company struggling to justify building a direct sales team to target 18,000 agencies is thrilled to use the platform of FirstNet’s App Catalog. That’s the best marketing money can buy! An important note here is that if you choose to rely on a curator (as an agency or a company), you better know what the curator is prioritizing. You want to be Breitbart using Facebook as a springboard in 2016, not today.

Today we are only seeing the beginnings of what AT&T hopes to do with FirstNet’s App Catalog - it will be fascinating to see how they strategically invest in it over time. Neither AWS nor Azure have given any signs of pursuing this kind of platform other than promoting tech firms that use their cloud infrastructure.

Value to Agency

Guidance - Too many choices can be a burden. Nice to know what the big dogs think, and if they can sweeten the deal as a bundler/reseller, that’s a bonus. It can also be a form of unbundling: FirstNet’s catalog of approved apps are simple, complementary forms of the software these companies sell individually. In a way, it’s a step towards selecting a public safety suite feature by feature with FirstNet as the marketplace.

Company Strengths:

Little risk, unless any of the four have designs on competing with the companies they support. In which case, it could get awkward.

Stripe, a payments platform, recently announced Stripe Capital, a service which extends financing to growing companies based on their history with Stripe. Because Stripe has proprietary and detailed data on the cash flow and growth of companies on their platform, they can make intelligent decisions on companies they want to back. In public safety, these four companies can build a similar model, where they decide what metrics indicate future success and can support growing companies on their platform.

Company Vulnerabilities:

The distance (moreso for cloud infrastructure providers) between their core businesses and agency operations complicates things. The prototypical customers for all of them are enterprise businesses and consumers, not public safety. FirstNet is closest, but still not representative of AT&T at large.

Who’s Doing It

AT&T FirstNet - Top Tier

Verizon Public Safety - Top Tier

Microsoft Azure - Top Tier

Amazon AWS - Top Tier

All the little cos who benefit - Honorable Mention

Buddy or Bust

Say you run a public safety tech company that does one (or maybe two) things very well, but you don’t anticipate expanding your product line. What should you do? There are a handful of decent, profitable, important businesses that are in this position: IAPro manages internal affairs investigations, PowerDMS and Lexipol do compliance and knowledge management, BluHorse is a standalone jail management system. What’s wrong with that? Nothing. It’s not a problem… yet. Your standalone product can go from product leader to existentially questionable very quickly, however, when a more strategically positioned company decides to come for your lunch. As explained in the PSaaS section, it’s effort-prohibitive for agencies to look for a different, individual solutions. Agencies are willing to get only 85% of their needs met if they can cut 70% of the procurement work.

If you’re dead set against being acquired, or want to hedge so growth isn’t off the table later, look to find complementary companies and partner. Build a strategic network of small companies, do the necessary work to integrate so data flows smoothly (easier said than done), discount bundles, and build incentives across sales orgs to cross-sell products within the network.

Value to Agency:

Best in Breed - There’s an inherent trust in working with a company that only serves your sector, and builds one or two products that address a specific need. Combining 3+ of those products gets you close to a full public safety suite.

Bundles, baby.

Company Strengths:

Able to focus on what the company does best.

Force multiplier for sales channels.

Company Vulnerabilities:

Dependencies outside company control are inherently risky. What happens if one partner gets acquired? Or goes out of business?

Product development roadmaps suddenly have more questions: will this update impact partners? Who do we need to include in strategic product decisions?

Who’s Doing It

Lightning Partnership (RapidDeploy, RapidSOS, Getac, Orion) - Top Tier

Axon, DJI, Cradlepoint - Second Tier

Closing Thoughts

You don’t have to commit to one strategy. In fact, several of them are mutually coherent and additive. For example, Motorola and Axon are both attempting to become full PSaaS companies, with Motorola well on its way. RapidDeploy built the Lightning Partnership, but that doesn’t mean they won’t enter additional public safety software markets and make a push to become a PSaaS. Nothing is stopping Esri or RapidSOS from attempting to make location data/services as foundational as cloud computing or LTE data, and becoming a curator of apps that sit on their own protocols.

Finally, I’ve been struggling to perfectly describe the interaction between bundling/unbundling and curation in these strategies. If curation requires an outside eye that is choosing complementary pieces, then only Comms Curator is a curator. You could make an argument that a thoughtful partnership is a form of curation as well. I don’t know if this diagram tells us anything useful, but it was the framework I kept falling back to in my head:

Thanks for reading. Send me feedback at mitchell@rollcall.media! If you enjoy this newsletter, please share it, forward it to your friends, or just sign up here.

-MA