Lessons from ShotSpotter (Subscribers)

Lessons from ShotSpotter (Subscribers)

pt. 1

Hi,

Welcome to Roll Call, a newsletter about the state of policy and technology in public safety, and the people shaping it. If you’d like to sign up, you can do so here. Or just read on…

TL;DR

ShotSpotter is undervalued in the short- to medium-term, but guns/homicides being required for the business model complicates the long-term.

Global firearm homicide data confirms ShotSpotter’s necessity, but proves that Latin America requires far more attention/effort than European ambitions. I hope they prove me wrong on international expansion! ShotSpotter can make a big difference in Central and South America.

ShotSpotter buying HunchLab was maybe the acquisition of 2018, and enables the use of bias-free gunshot data to lead on proactive/precision policing software.

Today is the first note on a specific company: ShotSpotter. We’ll highlight their unique advantages, weaknesses, and strategic position in the public safety landscape. I have spent a lot of my career thinking about bringing products to market and juicing sales teams, but I do not come from a finance-heavy background, so take that section with a grain of salt. This was a challenging and fun exercise in thinking about the incentives at play and the work it takes to build a company successful enough to be on a public stock exchange. I’m excited to do this for other companies and get better. Generally, these notes will be exclusively for paid subscribers. To show how these will be structured in all 40-50 notes in 2020, I’m making the first one free.

I chose Shotspotter as the first analysis subject for a few reasons. First, their product suite targets a massive public safety need. ShotSpotter’s Flex product is designed to help first responders get to gunshot victims faster, and increase the amount of evidence agencies have to prosecute repeat gun crime offenders. They’re also increasingly moving into topical markets like higher education campus protection and predictive policing. Second, they went public ($SSTI) relatively recently, so I could look at their S-1 and subsequent disclosure documents and get a good picture of their last 5 years. Third, the gunshot detection competitive landscape is changing fairly quickly, and I’ve always been curious if their early lead would prove a defensible moat or if other tools could quickly catch them.

Here we go:

The ShotSpotter Thesis

Short version: We believe that we can reduce community violence by focusing on guns, which are at the intersection of the worst and most preventable crimes.

Long version: Gun crimes will continue unless agencies attack the problem with a balanced approach, a critical piece of which is gunshot detection for (a) faster response and (b) expanded ballistic evidence collection to go after frequent shooters. We are also the company best positioned to proactively address the most current threats to schools, corporate campuses, and other targets of mass violence. Finally, the gunshot data we collect is the purest distillate of dangerous activity in neighborhoods, which means we can (carefully) predict without bias where and when gunshots are likely to occur and feed that information to first responders.

ShotSpotter’s purpose, in their own words:

“Earn the trust of law enforcement to help them provide equal protection for all and strengthen the police-community relationship, ultimately reducing gun violence.”

How Big is the Problem?

ShotSpotter helps municipalities and public safety agencies address gun crime. To do so, they do not sell a surveillance product like CCTV cameras, or a long-term gun replacement like Axon. To put it in human infrastructure terms, ShotSpotter manufactures and sells the eardrums of the city. To hear a gunshot and quickly locate it boosts the reaction time of first responders. Frankly, it’s impressive and praiseworthy; we’ll dig into it later. An unfortunate truth is that gunshot detection is wholly downstream of guns, unlike video surveillance or Tasers. Where cameras extend the eyes of a city and Tasers are force-delivery mechanisms parallel to firearms, ShotSpotter’s main product reacts to one specific, important kind of threat.

Both guns and homicides are a necessary condition for gunshot detection. If guns disappeared tomorrow, ShotSpotter would be out of business. If there are more homicides and cities become more dangerous, ShotSpotter (by no fault of their own) has a compelling case in the biggest 1,000 cities in America. I believe that this perverse incentive structure, however accidental, is a long-term weakness for the company.

That said, there is zero chance that guns are going anywhere, at least during the next 10-15 years in the United States. And the problem ShotSpotter addresses is global. We’ll explore the total addressable market in detail later, but ShotSpotter believes that 18% of their TAM is international, including 200 cities across Europe, South America, and Southern Africa. My gut told me that overweighted Europe and underweighted Latin America, but I’m a product of the unique firearm atmosphere and culture in the U.S. and my knowledge of the gun violence problem doesn’t extend far beyond our borders.

So I dove into the data. What does the gun violence problem look like globally? Where are the guns and how bad is the homicide problem? This question led me down the very sad rabbit hole of global firearm deaths, homicides vs. suicides, and the US. Dept. of State categorizing countries as ‘drug producing or transporting.’ I found this to be the best source on global mortalities from firearms. It is worth reading if you really want to make yourself sad, but I’ve pulled the most relevant findings here:

“Worldwide, it was estimated that 251,000 (95% uncertainty interval [UI], 195,000-276,000) people died from firearm injuries in 2016, with 6 countries (Brazil, United States, Mexico, Colombia, Venezuela, and Guatemala) accounting for 50.5% (95% UI, 42.2%-54.8%) of those deaths… The majority of firearm injury deaths in 2016 were homicides (64.0% [or 161,000 deaths]).”

“Aggregate firearm injury death rates decreased between 1990 and 2016 in most countries; however, rates increased in 41 countries, of which 3 were significant changes (20 of these increases were in the GBD super region of Latin America and the Caribbean).”

Almost all countries with firearm homicide rates of more than 10 per 100,000 persons were categorized by the U.S. Dept. of State as ‘drug producing or transporting’ (orange in chart below).

There are only twelve countries with more firearm mortalities per 100k persons that the United States, but almost thirty with a higher homicide rate. Most of the United States’ mortalities from gun violence are suicides (6.4 per 100k persons), with Greenland (22.0 per 100k) the only country worse than ours.

Western Europe combined has a firearm homicide rate of only .2 per 100k persons! Very few European cities will feel pressure to pay $1 million per year for a gunshot detection system that’s used 10 times a year.

Overall, the global gun violence problem is concentrated pretty heavily in the Americas: the U.S. as one of only seventeen countries with above median suicide and homicide rates, and Central/South America with most of the top thirty homicide rates. That said, it is certainly a problem worth solving and I’m glad ShotSpotter is taking it on.

Strategic Model

The diagram above is a callback to our explanation of the modern duty belt. ShotSpotter sits at the beginning of the call for service lifecycle. In fact, sometimes it preempts the cycle entirely: one statistic ShotSpotter often cites is that city residents call police less than 20% of the time shots are fired (Brookings 2016). Even if they do, ShotSpotter can notify public safety agencies on average 3-5 minutes before the call comes in. Emergency communications officers in a PSAP can visualize shots fired and dispatch law enforcement or EMS to the scene quickly. A forensic report is generated for incidents that are given CFS numbers, which are court-acceptable.

Products

ShotSpotter Flex: The main product, and 97% of 2018 revenue. 15-20 sensors per square mile, which are triggered by the sound impulse of a gunshot. Location of the gun is then triangulated between multiple sensors. Software for visualization, alerts, and data retention.

Value Prop: Multifaceted. First, the economic value of homicide prevention. ShotSpotter’s 2018 10-K says that according to a 2016 Urban Institute report, “one fewer gun homicide [in Minneapolis] in a given year was statistically associated with the creation of 80 jobs and an additional $9.4 million in sales across all business establishments in the next year.” “In Oakland, every additional gun homicide in a given year was statistically associated with five fewer job opportunities in contracting businesses in the next year.” “In Washington, D.C., every additional gun homicide in a given year was statistically associated with two fewer retail and service establishments the next year.” Second, Flex decreases pre-hospital time for gunshot victims, according to this journal article. The same article, however, surprisingly caveats that “mortality, when adjusted for distance, Trauma, and Injury Severity Score, Injury Severity Score, and shock index, was not significantly different between ShotSpotter and non-ShotSpotter incidents.” Faster treatment, but not necessarily lives saved. Third, there’s anecdotal evidence that when applied as part of a city-wide gun violence reduction strategy, it helps lead to arrests of frequent shooters.

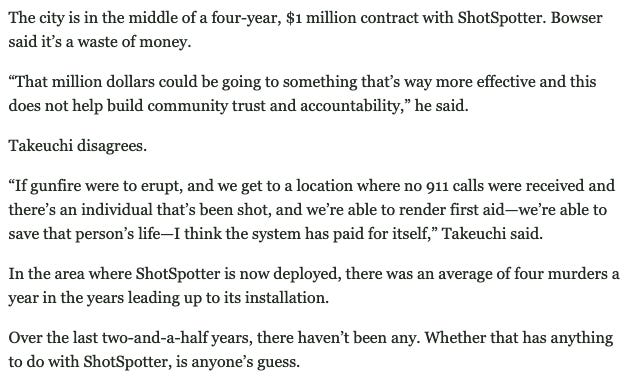

Complexity: Entangled. Let’s expand that third point about ShotSpotter being part of a broader strategy. Below is a clip from this KPBS San Diego article, published in mid-2019:

Four murders per year is too many. San Diego has taken large steps towards addressing a problem, a piece of which is purchasing and installing ShotSpotter Flex. An earlier Roll Call post raised the product-management-level difficulty in public safety of attributing lives saved to a specific product. It’s too messy. One more thing to say here: there’s an awesome question/answer on the value-add of NIBIN (Nat’l Integrated Ballistic Imaging Network) to agencies that use it in conjunction with ShotSpotter from the Q3 Earnings Call that is worth reading (pg 10).

ShotSpotter Security: Flex, but serving university and corporate campuses. Includes 20-30 sensors per square mile.

Value Prop: Use cases geared specifically for higher education or private security users. In June 2018, strategically discontinued indoor gunshot detection due to a lack of interest.

Complexity: WYSIWYG. It’s Flex, but for the private sector. I’d posit that the “1,626 public colleges, 1,687 private nonprofit schools,” (USNews) and Fortune 500 headquarters are the most likely targets, which is just under 4,000 opportunities - less than the 5,000 campuses in ShotSpotter’s stated TAM.

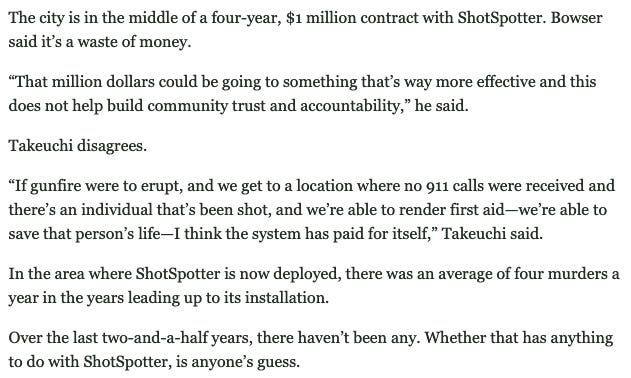

ShotSpotter Missions: What ShotSpotter has called their acquisition of HunchLab, which they bought from Azavea in 2018. Azavea called it a “crime risk forecasting system” using location and historical crime data.

Value Prop: Underrated. Frankly, this is where I’m most excited about the potential of ShotSpotter, at least in the United States. Predictive policing (rightly) gets a bad rap, and attempts to do so should be heavily scrutinized by both public sector buyers and the city neighbors it affects. But HunchLab, or Missions, in the hands of ShotSpotter is a good thing. A couple reasons: first, they got the buy-in from the Azavea team. The company is dedicated to civic and social impact, so their vote of confidence means a great deal. Second, ShotSpotter’s big value-add to what they call ‘precision policing’ is true, unadulterated gunshot data. Gunshots! The evidentiary signature of danger! ShotSpotter claims that there’s inbound interest in their Missions product separate from their Flex product. They should not pursue those opportunities; there would be no difference between them and the PredPols and Palantirs of the world. Gunshot data is truly unbiased, truly dangerous, and likely has some predictive power. This is compelling, and worth more as an upsell than they’re pricing it ($50k per year).

Complexity: Noted above. If ShotSpotter mostly sees this as a pathway to crime intelligence contracts instead of an add-on to a gunshot detection system, that’s a recipe for trouble. It also requires integrating with other companies’ dispatch (CAD) and records (RMS) software systems to provide the full picture of historical crime data.

Competitive Landscape

Utility - The company, best known for a bodyworn camera system built around the capabilities of a smartphone, recently announced that they were bringing Active Shooter Response Technology to market. Their ASRT is the first direct competitor in spatial, acoustic gunshot signature detection. It’s marketed as something of a hybrid between Flex and Security, with most of Utility’s examples as campuses or businesses.

PredPol / Palantir - Companies known for predictive policing software. They don’t have the luxury of unreported gunshot data, but they do have the name recognition of law enforcement focused software providers.

Wi-Fiber - Recently beat ShotSpotter for a contract in Canton (OH), where ShotSpotter was hoping to renew. If IoT means the capacity for other companies to add Flex features on other municipal tools (like street lights, in this case), that could be bad news for ShotSpotter.

Citizen - A consumer app, but pulls basically all data off police scanners onto a live, visual platform. It also has user-generated content, in that you can hear a gunshot, record an incident, post it, and it will be connected to the call for service generated by Citizen. Included here because reaction time to gunshots is probably faster than 911 calls, but just slower than ShotSpotter.

Second Order Competition

Motorola Solutions - Has been on a spree of acquisitions over the last few years. Two of those are included here, in Avigilon and Spillman. Avigilon is their CCTV or static camera software. Motorola (and the CCTV providers below) is included because the number of static surveillance cameras in cities is rising dramatically, and it doesn’t seem farfetched for providers to add audio capability to their cameras. Doing so would double their value for cities/neighborhoods and cut ShotSpotter out. Spillman is a CAD/RMS provider that, coupled with the features already in Motorola’s solution, provides meaningful insight into historical crime. Remember, ShotSpotter Missions requires a foundation of CFS (call for service) and crime data before gunshot data adds value.

Genetec / Flock Safety - As mentioned above. Video and audio likely trumps audio, despite their lead in gunshot recognition. CCTVs by city

Central Square / Tyler Tech - Like Motorola and Spillman, these are a couple of the major players in CAD and RMS. They have massive cash flow to throw around, and have their own criminal data sets on which to build predictive models.

Business Model

Subscription-based SaaS revenue, with deployment costs spread over contract. Past initial contract, option years escalate in cost. The Miami-Dade contract is a good example.

$10k per square mile service initiation and startup fee

$65k per square mile per year licensing, hosting, and maintenance

+ hardware costs

Paid in equal monthly installments for a sum of $3.41M over first 5 years

Risks

2017 S-1: “The majority of our installed ShotSpotter sensors use third-generation, or 3G, cellular communications and we will continue to deploy 3G enabled sensors in 2017. Certain wireless carriers have advised us that they will discontinue their 3G services in the future and our ShotSpotter sensors will not be able to transmit on these networks. We will have to upgrade the sensors that use 3G cellular communications at no additional cost to our customers prior to the discontinuation of 3G services, the timing of which is uncertain. These sensor replacements will require significant capital expenditures and may also divert management's attention and other important resources away from our customer service and sales efforts for new customers. We are currently developing a ShotSpotter sensor that will use fourth-generation (4G) Long-Term Evolution (LTE) wireless technology.”

- 2018 10-K: “Starting mid 2020 through 2022 we will have to upgrade our sensors that use third-generation cellular communications to the fourth-generation Long-Term Evolution wireless technology, which will increase our cost of revenues.”2017 S-1: “We rely on a limited number of suppliers and contract manufacturers. In particular, we use a single manufacturer, with which we have no long-term contract and from which we purchase on a purchase-order basis, to produce our proprietary ShotSpotter sensors. Our reliance on a sole contract manufacturer increases our risks since we do not currently have any alternative or replacement manufacturers, and we do not maintain a high volume of inventory. In the event of an interruption from a contract manufacturer, we may not be able to develop alternate or secondary sources without incurring material additional costs and substantial delays. Furthermore, these risks could materially and adversely affect our business if our contract manufacturer is impacted by a natural disaster or other interruption at a particular location because each of our contract manufacturers produces our products from a single location. Although our contract manufacturer has alternative manufacturing locations, transferring manufacturing to another location may result in significant delays in the availability of our sensors.”

2017 S-1: Many of the key components used to manufacture our proprietary ShotSpotter sensors also come from limited or sole sources of supply. Our contract manufacturer generally purchases these components on our behalf, and we do not have any long-term arrangements with our suppliers. We are therefore subject to the risk of shortages and long lead times in the supply of these components and the risk that suppliers discontinue or modify components used in our products. In addition, the lead times associated with certain components are lengthy and preclude rapid changes in quantities and delivery schedules. Developing alternate sources of supply for these components may be time-consuming, difficult, and costly, and we or our suppliers may not be able to source these components on terms that are acceptable to us, or at all, which may undermine our ability to fill our orders in a timely manner.

Key Metrics

At the time of writing, ShotSpotter’s ($SSTI):

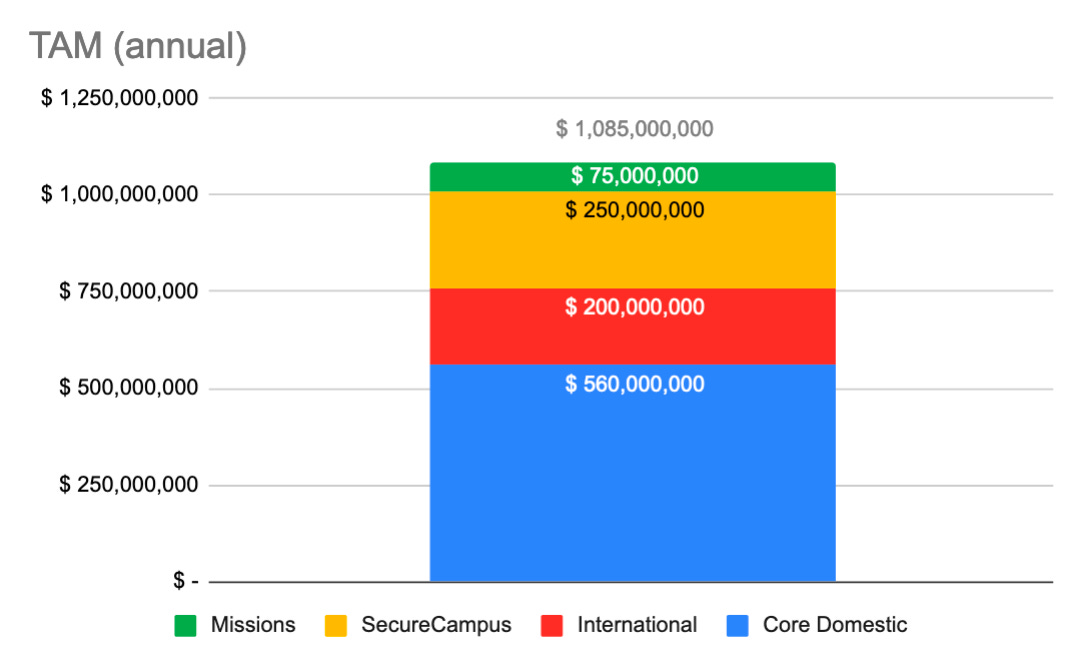

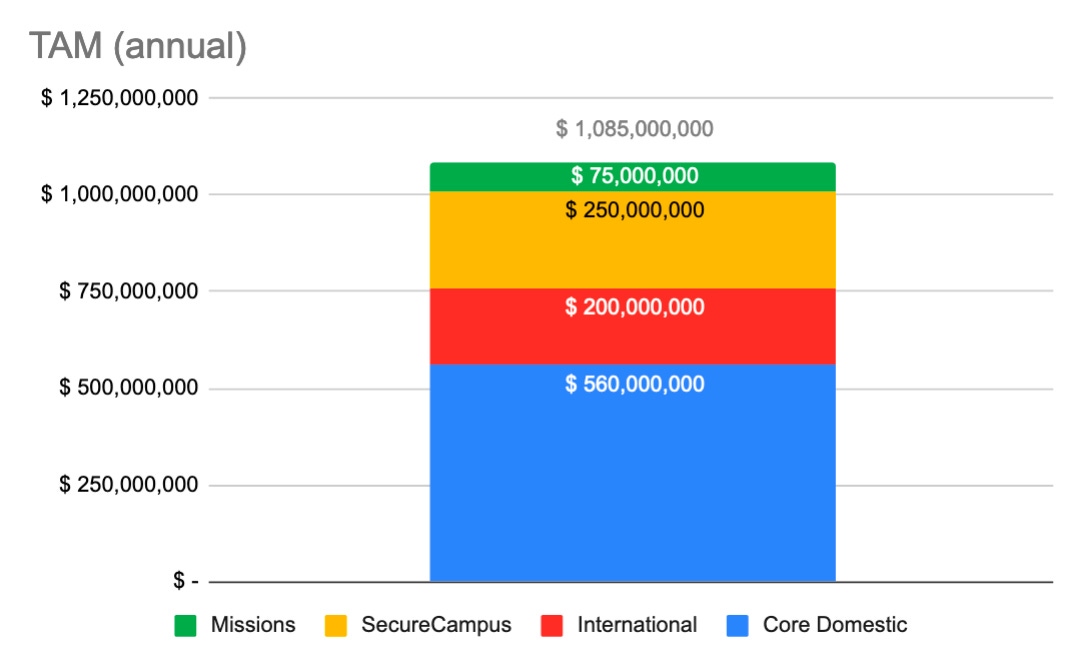

TAM (per ShotSpotter) - $1.085B

TAM (estimated by me) - $910M (equal Core, less $100M Int’l, less $150M Secure, plus $75M Missions)

Market cap - $325.26M

Valuation multiple - 9.36 x rev (2018)

(Comps: Motorola Solutions ($MSI) - 3.98, Axon ($AAXN) - 10.26)Average Order Value (as of Dec 2018) - ~$347,530

More data in the section below (coverage, customers, employees, etc.)

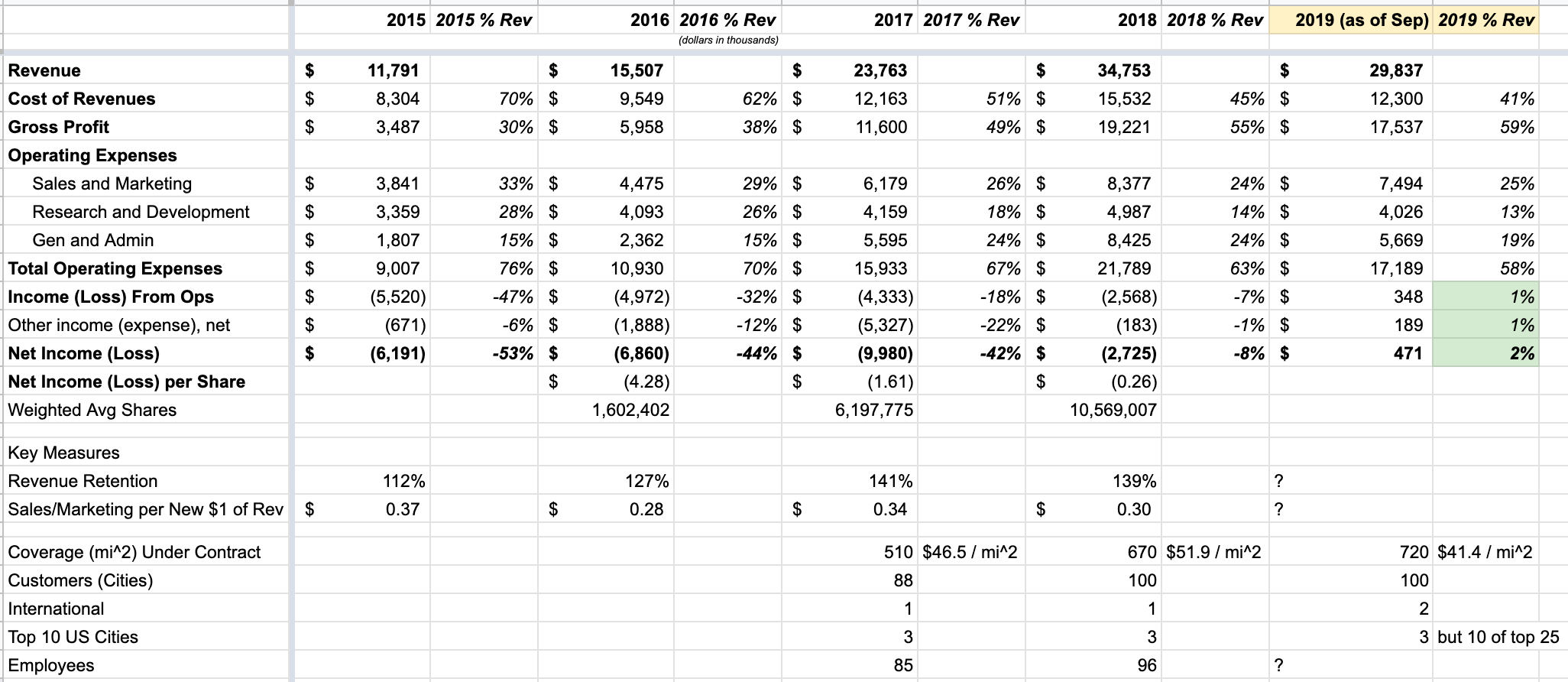

Financials

Key Players

The two questions that matter most:

Can ShotSpotter position themselves as a leader in solving the gun violence problem (yes) while positioning themselves for a post-gun-violence future in the United States (unknown)? Only Ralph Clark knows.

Can ShotSpotter finally break into Latin America (unknown)? Only Jon Magin knows.

Frankly, I’m not sure. This slide of their 2019 Investor Day deck worries me:

Ralph Clark - CEO, President

Jon Magin - VP Int’l Sales, Latin America

10 Open Roles (Public)

Product

Director of Mission Solutions

Director of Security Solutions

Sales

Account Exec x2

Pro Services

Implementation Specialist

Customer Success

Director of Customer Success x2

Engineering

Technical Support Engineer

Software Eng - Missions

Reference Docs

Material I wanted to read but couldn’t:

Translations and Translation Gaps (2018) by Leonardo Cardoso, about ShotSpotter’s short-lived time in Brazil and what went wrong (from a linguistic point of view)

Thanks for reading. Send me feedback at mitchell@rollcall.media! If you enjoy this newsletter, please share it, forward it to your friends, or just sign up here.

-MA

Recommended Reading

Staring at Hell by Kate Wagner

A brutal short story, The Ones Who Walk Away from Omelas, by the great Ursula K. Le Guin